Creation of the document acceptance for accounting wasps. Creation of a document acceptance for accounting of wasps Accept equipment for accounting 1s

Fixed assets are inventory items with a value of more than a certain amount (constantly increasing) and the useful life of which is more than a year.

Fixed assets include buildings, structures and other real estate, construction projects, equipment, power lines, pipelines, and so on.

In the 1C 8.3 system, several separate sections are allocated for accounting for fixed assets, which contain all the necessary operations for full-fledged work on this topic:

- Chapter " Receipt of fixed assets". In this section, you create documents for which are included in the cost of fixed assets. Also in this section, 1C is drawn up.

- In chapter " Accounting for fixed assets» you can create documents that reflect the movement and inventory of fixed assets.

- Chapter " Disposal of property, plant and equipment» contains documents on the write-off and transfer of fixed assets.

- Chapter " Depreciation of fixed assets» is responsible for depreciation calculations and accruals.

In this article, using a cross-cutting example in the form of step-by-step instructions, we will consider the basic operations related to accounting for fixed assets in 1C 8.3.

Receipt can be in the organization () and leasing. In this article, we will consider accounting for acquired fixed assets.

So, let's create an OS posting document. I will not dwell on the creation of the receipt document in detail, since there is a topic on this topic. I will give only an example of a formalized document to make it easier to move on:

Receipt of additional expenses for fixed assets

The initial cost of equipment and other items of fixed assets is formed at the acquisition stage not only from the purchase price, but also based on installation costs and other costs associated with the acquisition.

Therefore, it is worth considering two documents:

- Transfer of equipment for installation.

You can create them in the section "Fundamental assets and intangible assets" - Receipt of fixed assets. As usual, documents are created by clicking on the "Create" button. In the header of the document, typical details are filled in - Organization and Counterparty.

In the tabular part, in the "Main" tab, the amount of additional expenses is indicated:

On the “Goods” tab, an item of fixed assets is indicated, in the cost of which these costs are included:

Our video about the receipt of additional expenses in 1C Accounting:

Get 267 1C video lessons for free:

Transfer to installation

In this document, fill in the following details:

- Organization.

- Stock.

- Construction object.

- Cost item.

Let's add the equipment to the tabular part:

The above documents must be created before the fixed asset is taken into account.

How to register and put into operation OS

This procedure has already been described by me earlier. I will not describe again, I will only show how the document is filled out, and I will say that as a result of the document, the equipment is transferred from account 08.04 to account 01.01.

Tab Non-current asset:

OS tab:

Depreciation in transactions will be charged to account 02.01:

Our video about the receipt and acceptance for accounting of a fixed asset in 1C 8.3:

Moving OS to 1C

Moving a fixed asset is very similar to moving goods, only the goods are moved between warehouses, and the fixed asset is moved between departments (after all, we have already taken it into account).

When drawing up a document, questions can only be caused by the details “Depreciation calculation” and “Method of reflecting depreciation expenses”.

These details should be specified if depreciation needs to be charged after the transfer. We will leave them blank, and we will accrue depreciation at the end of the month:

Inventory of fixed assets

The inventory of fixed assets in 1C practically does not differ from the inventory of goods, only, again, instead of the warehouse, we indicate the unit (more about goods in the article). In the tabular part, instead of the quantity, we indicate the sign of the presence of a fixed asset:

In the event that the fixed asset is not listed in the accounting, but in fact it is, on the basis of the inventory, a document of acceptance for accounting is made, and vice versa, if it is actually absent, we write off.

Here, in addition to the standard fields, we indicate the reason why the fixed asset is written off:

We will not post the document, since we will still need the fixed asset to consider the depreciation operation.

Depreciation of fixed assets

Calculation and reflection in accounting is done using the month closing assistant. The operation is done once a month and, as a rule, at the end:

To open the assistant, you need to go to the "Operations" menu, then follow the link "". An assistant window will open immediately. In it you need to select the period and organization. Then the assistant will do everything himself. All calculations in the assistant are made sequentially, and depreciation is calculated first. If the operation was completed without errors, a document of the scheduled operation "Depreciation and depreciation of fixed assets" will be created:

Fixed asset accounting is a section of accounting that concerns almost every institution. And sometimes even simple OS accounting operations raise questions from accountants. In this article, I would like to tell you how to reflect in accounting the fact of purchasing a fixed asset using the program "1C: Accounting of a state institution 8, edition 2.0".

As you know, the purchase of fixed assets is not carried out directly to the accounts of group 101.00 "Fixed assets". First, the fixed asset and the costs of its delivery, assembly and any other associated costs are accumulated on the accounts of group 106.00 “Investments in non-financial assets” (if these are fixed assets that are actually already on the territory of the institution) and group 107.00 “Non-financial assets in transit ” (if these are fixed assets that are on the way). It is not recommended to keep capital investments in fixed assets on accounts 106.00 for a long time, so that in case of verification there are no unnecessary questions. Although such situations are very rare in practice: the acquired fixed asset is most often immediately taken into account, except for long-term investments in capital construction.

The section on working with fixed assets in the program "1C: Accounting of a state institution 8, edition 2.0":

The section includes various directories, documents and reports intended for accounting for fixed assets:

In order to start reflecting the fact of receipt, you must use the document of the same name:

Again, different documents are used for fixed assets actually delivered and fixed assets in transit. And when registering the document for the receipt of fixed assets, intangible assets, intangible assets, the fixed asset in which was previously issued to the group account 107.00 (as a fixed asset on the way), it is better to use the input mechanism on the basis. Let me explain: if you are waiting for some fixed asset that is still on the way, then reflect this fact with the document “Receipt of fixed assets (on the way)”. After this fixed asset has arrived - on the basis of the previously entered document “Receipt of fixed assets (on the way)”, we enter the document “Receipt of fixed assets, intangible assets, intangible assets”. This is methodically correct and will simplify your task - most of the details will be filled in automatically.

In our example, consider the reflection in the accounting of a fixed asset that has already been actually delivered and the purchase of which will be reflected in the accounts of group 106.00:

Let's use the standard button to create a new document:

The form for filling out the document opens:

Almost any document in the 1C: BSU 8 program consists of a header:

And tabular parts, designed in the form of tabs:

Let's fill in the header of the document (the "Agreement" field is not available for editing until the counterparty is selected):

There is also a field in the header - advance payment offset:

In this field, you can select the advance payment option:

By default, it is set to "Automatic" - this means that if the advance payment was paid to the supplier in advance, the program will select it and automatically offset it. When you select this option on the "Advances offset" tab, the form is empty:

The status "By document" means that the user can manually select the document for the advance payment to the supplier, as well as the amount that needs to be credited. When this state is selected, the form also changes:

Also in the header of the document there is a hyperlink on VAT, but since the VAT deduction is the topic of a separate article, we will not dwell on it in detail.

Let's go back to the first tab. On this tab, information about the capital investment is filled in. In the tabular section, using the "Add" button, fill in the necessary credentials:

Since our example is excluding VAT and the fixed asset is purchased new, the columns of the same name are not filled in:

The column "Transferred depreciation" is filled in if there is already some accumulated depreciation for this fixed asset.

Next three tabs:

These tabs must be filled in if the document registers the receipt of equipment, since the printed form of the equipment receipt certificate is filled out on the basis of these tabs. In our example, the fixed asset being purchased is not equipment, so we will leave them blank.

The last and most important tab of the form is Accounting Transaction. This tab determines which postings will be generated after the document is posted. In our example, the typical operation string is empty, which means that more than one operation can be selected in this document:

Until the operation is selected, there are no other details on the form.

Consider the operations that can be used in this document:

Operations with clarification (obsolete) do not need to be used, these are old operations that are necessary only for the formation of turnovers of past periods (after all, these operations were once used).

The following two operations for gratuitous receipt (receipt without cash costs):

There is also an operation on the list:

This transaction is used to record the purchase of a fixed asset through an accountable entity.

Last operation in the list:

This operation is just used when creating a document to reflect the receipt of a fixed asset, previously accounted for as fixed assets on the way.

In our example, we use the following operation:

This operation is applied when OS is received from suppliers.

When you select an operation, the appearance of the form changes slightly, additional details of the operation appear, which must be filled in:

Separately, I will talk about tax accounting. Often, tax accounting in public institutions is simplified or not carried out at all in the program. Therefore, this requisite is optional for filling:

Separately, I note that the program has the ability to immediately accept monetary obligations in the document:

Very convenient functionality for generating postings on accounts of the five-hundredth group:

After posting the document, it is necessary to check the resulting postings. There is a special button on the document form for this purpose:

The first entry concerns monetary obligations: this document accepted monetary obligations for the entire amount of the cost of the fixed asset, since in our example the advance payment was not paid (remember that monetary obligations are accepted separately before the advance payment):

The second posting is the accrual of capital investments for the entire amount of the cost of the fixed asset:

The third posting concerns tax accounting. Special tax accounts were used to maintain such records:

After the purchase of a fixed asset has been recorded, it is also possible to collect all associated costs in the capital investment account to reflect the true value. For example, in addition to paying the cost of the OS, we also paid for shipping.

This fact is reflected in the document:

Create a new document:

Fill out the document:

We will select the required typical operation and fill in additional details (accordingly, the operation we need should reflect the fact of investments in the fixed asset), we will also simultaneously accept monetary obligations:

After posting, the document generates the following account movements (absolutely similar in composition):

After our manipulations, we will check the result of the work in the report "Turnover balance sheet":

The result is a debit balance on account 106.31 and a credit balance on account 502.12:

In one of the following articles, we will consider how to take into account a fixed asset, the costs of which are collected on group account 106.00.

In 1C, there are two options for registering the acquisition and accounting for the OS:

Standard, which uses two documents:

- capitalization of the OS - using a document Receipt (act, invoice) type of operation Equipment ;

- OS commissioning - using the document Acceptance for OS accounting .

Simplified, in which a single document is used:

- posting and commissioning of OS - document Receipt (act, invoice) type of operation fixed assets .

When the commissioning of the OS is carried out simultaneously with the posting of the OS, then, of course, it is more convenient to reflect all operations in one document: use Simplified version. But it has some limitations.

The simplified option cannot be used if additional costs are added to the initial purchase price of the fixed asset when it is acquired.

How to take the OS into account in 1C 8.3: the standard way

With the standard method, two documents are drawn up for the acceptance of fixed assets for accounting:

- document Receipt (act, invoice) type of operation Equipment ;

- document Acceptance for OS accounting ;

Consider the features of filling out each document and their implementation.

Document Receipt (act, invoice) type of operation Equipment

You can register the capitalization of the fixed asset with this document through:

- Purchases - Purchases - Receipt (acts, invoices) - Receipt - section Equipment;

- Fixed assets and intangible assets - Receipt of fixed assets - section Receipt of equipment.

So, for example, it is recommended to purchase a car that we plan to use on public roads in 1C Accounting 8.3 through the standard option, because the initial cost of the car will include additional costs - in this case, the fee for its registration with the traffic police.

On the tab Equipment enter the acquired fixed assets and indicate their quantity. Objects of fixed assets, select from reference book Nomenclature.

When posting the document, the initial cost of a non-current asset will be taken into account on the account "Acquisition of components of fixed assets" until it is entered document Acceptance for OS accounting.

Learn more:

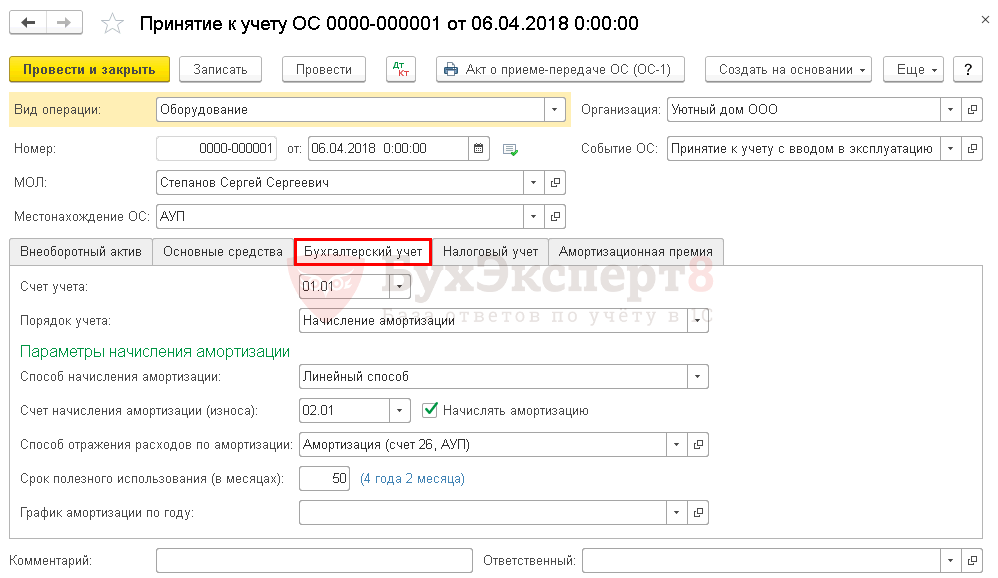

Document Acceptance for OS accounting

You can take into account the fixed asset with this document through:

- Fixed assets and intangible assets - Receipt of fixed assets - section Acceptance for accounting of fixed assets.

On the tab Non-current asset indicate the details of the acquired asset before commissioning:

- Equipment - non-current asset put into operation; choose from reference book Nomenclature;

- Main warehouse - the place of storage of the credited object;

- Check- cost accounting, where the initial cost of the object is formed.

On the tab fixed assets select OS to be commissioned from the directory fixed assets .

Set the parameters for depreciation, repayment of the cost of objects on separate tabs Accounting and tax accounting .

On the tab Accounting indicate:

- accounting account- account of the accounting put into operation OS;

- Accounting procedure

:

- Depreciation;

- The cost is not redeemed.

When choosing a value Depreciation set the parameters for its calculation.

On the tab tax accounting install .

Depending on the procedure for accounting for the costs of acquiring an object in NU in the field The procedure for including the cost in the composition of expenses can choose:

- Depreciation- for fixed assets for which depreciation will be charged;

- Inclusion in expenses upon acceptance for accounting- for objects, the cost of acquiring which at a time will be included in the costs when they are accepted for accounting;

- The cost is not included in the costs- for objects, the costs of which will not be taken into account in the costs that reduce the taxable base.

For NU in the document, it is impossible to select the depreciation method, because it is set in the accounting policy settings and applied to all OS objects. In 1C, the method is installed in the block Main - Settings - Taxes and reports - Income tax section.

For objects for which depreciation is charged, it is possible to charge a depreciation bonus. Its parameters are set on a separate tab. Depreciation premium .

The document generates postings:

Learn more:

- OS commissioning

- Acceptance for accounting of fixed assets that are not accounted for in NU

How to register an OS in 1s 8.3: a simplified way

With a simplified method, a single document is drawn up for the acceptance of fixed assets for accounting:

- document Receipt (act, invoice) type of operation fixed assets .

Document Receipt (act, invoice) type of operation Fixed assets

You can register a fixed asset with this document through:

- Purchases - Purchases - Receipt (acts, invoices) - Receipt - Fixed assets section;

- Fixed assets and intangible assets - Receipt of fixed assets - section Receipt of fixed assets.

In the tabular part, reflect the acquired objects from reference book Fixed assets. It is not possible to indicate the number of objects in the document: only one position in the amount of one object can be taken into account. Add the same items of fixed assets to the directory fixed assets separate positions and differentiate them according to certain characteristics, for example, by workplaces (WP).

According to the parameters of depreciation, repayment of the cost of objects, it is possible to specify only:

- Method of reflection of depreciation expenses in the document header - the same for all input objects;

- Life time in the tabular part - the useful life, which is set the same for NU and BU, specifically for each object.

1C Accounting 8.3 itself in tax accounting determines the procedure for paying off the cost of the acquired object:

- if the cost of the object is not more than 100,000 rubles, the acquisition costs are included in the costs at a time;

- if the cost of the object is more than 100,000 rubles, then depreciation will be charged in accordance with the method established in the accounting policy for NU.

Regardless accounting accounts in the tabular part of the document, the costs of acquiring fixed assets will be automatically taken into account on the account “Acquisition of fixed assets”, and then debited to accounting account set in the document.

The received fixed asset (car, building, machine, etc.) must be taken into account in order for VAT from its acquisition to be reflected in the purchase book, and.

The document "Receipt (acts, invoices)" generates the posting 08.04 - 60.01, which means its receipt at the warehouse. In order to correctly accept the OS for accounting in 1C 8.3 Accounting, a second posting is required from account 08.04 to 01.01. It is she who is formed when it is taken into account.

It is important to remember that in 1C 8.3 Accounting 3.0, starting from 2017-2018 (version 3.0.45), the developers greatly simplified this procedure by introducing a new type of operation "Fixed assets" for the document "Receipt (acts, invoices)".

When registering a receipt in this way, the document generates both postings, that is, it is not necessary to additionally take the fixed asset into account. The fixed asset will immediately be credited to the account on 01.01. You can read more about this type of operation in the article "".

In this example, we will consider the situation when you issued a receipt with the transaction type "Equipment". In this case, you have formed only one posting - on account 08.04. We also need to place the OS on account 01.01.

In the menu "FA and intangible assets" select the item "Acceptance for accounting of fixed assets".

In the opened document list form, click on the "Create" button.

In the header, indicate the financially responsible person and the location of the OS, but these fields are not mandatory.

On the first tab of the document, fill in the method of receipt and division. In the equipment field, select the stock item for which the receipt was previously created. The account will be filled in automatically, but it can be changed.

fixed assets

Next, go to the Fixed Assets tab. Add all required operating systems to the table. The inventory number will be substituted by default from the attribute of the directory of the selected OS. It can be changed and then when the document is posted, it will also change in the directory.

It's important to know! If you need to add several identical fixed assets (for example, 5 fixed assets), then you must have 5 such items with different inventory numbers in the fixed assets directory.

Accounting and depreciation parameters

Go to the "Accounting" tab. By default, during commissioning in 1C 8.3, the account 01.01 was substituted. We will not change this value. In the attribute “Accounting procedure”, set the value “Depreciation calculation” and the setting of depreciation calculation parameters will become available.

By default, the straight-line method of accounting for depreciation will be substituted. This method is the most common. When using it, the cost of the accounting object during the service life is reduced in equal parts.

Fill in the depreciation account, useful life and other fields. They shouldn't be a problem.

tax accounting

Go to the "Tax Accounting" tab. Indicate the initial price of fixed assets at NU, the date of purchase and the number of months of useful life.

Our organization is on the simplified tax system, so it is important to correctly indicate the procedure for including costs in expenses. It shows whether fixed assets are depreciated and how such expenses are accounted for.

Below you must specify the data on payments for all expenses before the object was accepted for accounting. All further payments must be made using the document "Registration of payment of fixed assets and intangible assets".

With other taxation systems, you do not need to specify the payment. You will have to indicate the depreciation premium - the percentage of the cost of the fixed asset that can be written off for its construction or purchase.

See also the video on how to buy an OS and register it:

I propose to consider in this article a detailed example of accepting fixed assets for accounting in 1C 8.3 in the form of step-by-step instructions. The accounting procedure for such assets is determined by PBU 6/01 “Accounting for fixed assets”.

When purchasing a fixed asset, an accounting entry is generated 08.04 – 60.01 (detailed -). It follows from this that the equipment is simply listed “in stock” on account 08.04 “Acquisition of fixed assets” and is not operated, and depreciation is not charged on it.

In order for the purchased equipment (machine, car, computer, etc.) to be listed as a fixed asset in the organization and depreciated, it is necessary to correctly take it into account.

Let's figure out what it means to take into account in 1C 8.3. From an accounting point of view, this means that it needs to be moved from account 08.04 to account 01.01 “Fixed assets in the organization”. The program still needs parameters for calculating depreciation both in accounting and in.

For all this, there is a document "Acceptance for OS accounting". Let's consider it in more detail.

Creating and filling out the document "Acceptance for accounting of fixed assets"

To create a new document, go to the menu "OS and", then click the link "Acceptance for OS accounting". A window with a list of documents will open. In this window, click the "Create" button. A window for creating a new document will appear:

In the header of the document, we indicate the organization, division (location of the OS), the financially responsible person and the event of the OS.

Get 267 1C video lessons for free:

Let's move on to the first tab "Non-current asset". We select the equipment that we want to take into account. We also indicate the warehouse where it is stored.

On the "Fixed Assets" tab, we collect a list of fixed assets to be accepted for accounting. In our case, this will be one line that matches the equipment:

In addition to choosing a fixed asset, you need to assign an inventory number on this tab. By default, this number is automatically substituted from the "Fixed Assets" directory (the "Directories" menu, then the "Fixed Assets" link).

Briefly about this directory: it stores all the parameters of the fixed asset and changes documents during operation.

For example, we can change the inventory number in our created document, which was taken from the directory. After posting the document in the directory, this number will also change. Entries in such a directory are also called fixed asset cards.